Best Credit Monitoring Apps 2025: A Complete Guide Based on Real Usage

Look, I’m gonna be honest with you right off the bat. I used to be one of those people who checked their credit score maybe once a year when I remembered, usually right before applying for something important. Then I got that lovely notification that someone had opened three credit cards in my name while I was blissfully unaware, binge-watching Netflix.

That was my wake-up call.

So for the past two years, I’ve been testing pretty much every credit monitoring app out there. Some are amazing, some are complete garbage, and some fall somewhere in the middle where they’re… fine, I guess? Anyway, here’s what I’ve learned from actually using these things day-to-day.

Why You Actually Need This Stuff

Here’s the thing about credit monitoring – it’s not just about knowing your score went up 5 points because you paid off that Target card. It’s about catching the weird stuff before it becomes a massive headache.

Last month, my Credit Karma app pinged me at 2 AM (yeah, I keep notifications on) about a hard inquiry I didn’t recognize. Turned out someone was trying to open a car loan with my info. Caught it early, filed the disputes, problem solved. Without monitoring? I probably wouldn’t have noticed until my score tanked.

Credit scores are based on complex algorithms that even financial experts debate about. The credit scoring system has evolved significantly over the years, but the basic principle remains: lenders want to know if you’ll pay them back.

The Apps I Actually Use (And Why)

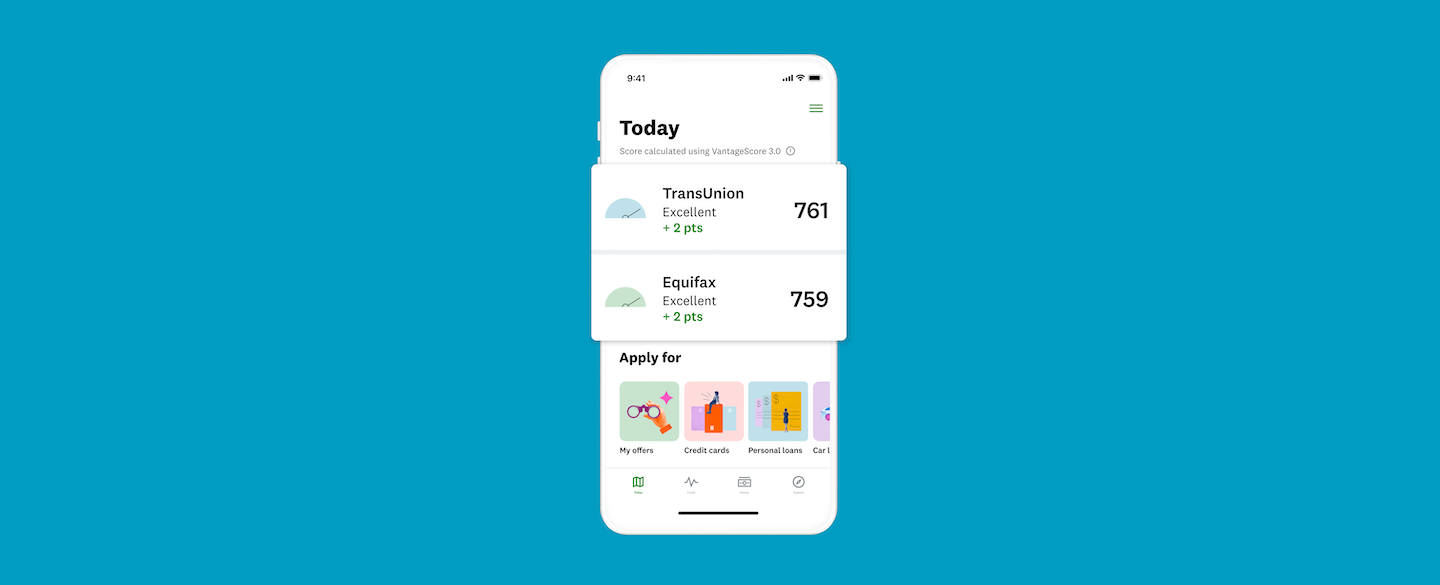

Credit Karma – The Free Favorite That Actually Works

Okay, so Credit Karma gets a lot of flak for not showing “real” FICO scores, but honestly? For free monitoring, it’s pretty solid. I’ve been using it for three years now, and the alerts are usually spot-on.

The interface is clean – maybe too clean sometimes, like they’re trying really hard to look friendly and non-threatening. But whatever, it works. You get scores from TransUnion and Equifax, which covers most of what you need to know.

What I Like:

- Actually free (no hidden fees)

- Alerts come fast – usually within 24 hours

- Credit card recommendations aren’t terrible

- Tax filing integration is handy

What Bugs Me:

- VantageScore vs FICO can be confusing

- Lots of credit card ads (I get it, gotta make money)

- No Experian data

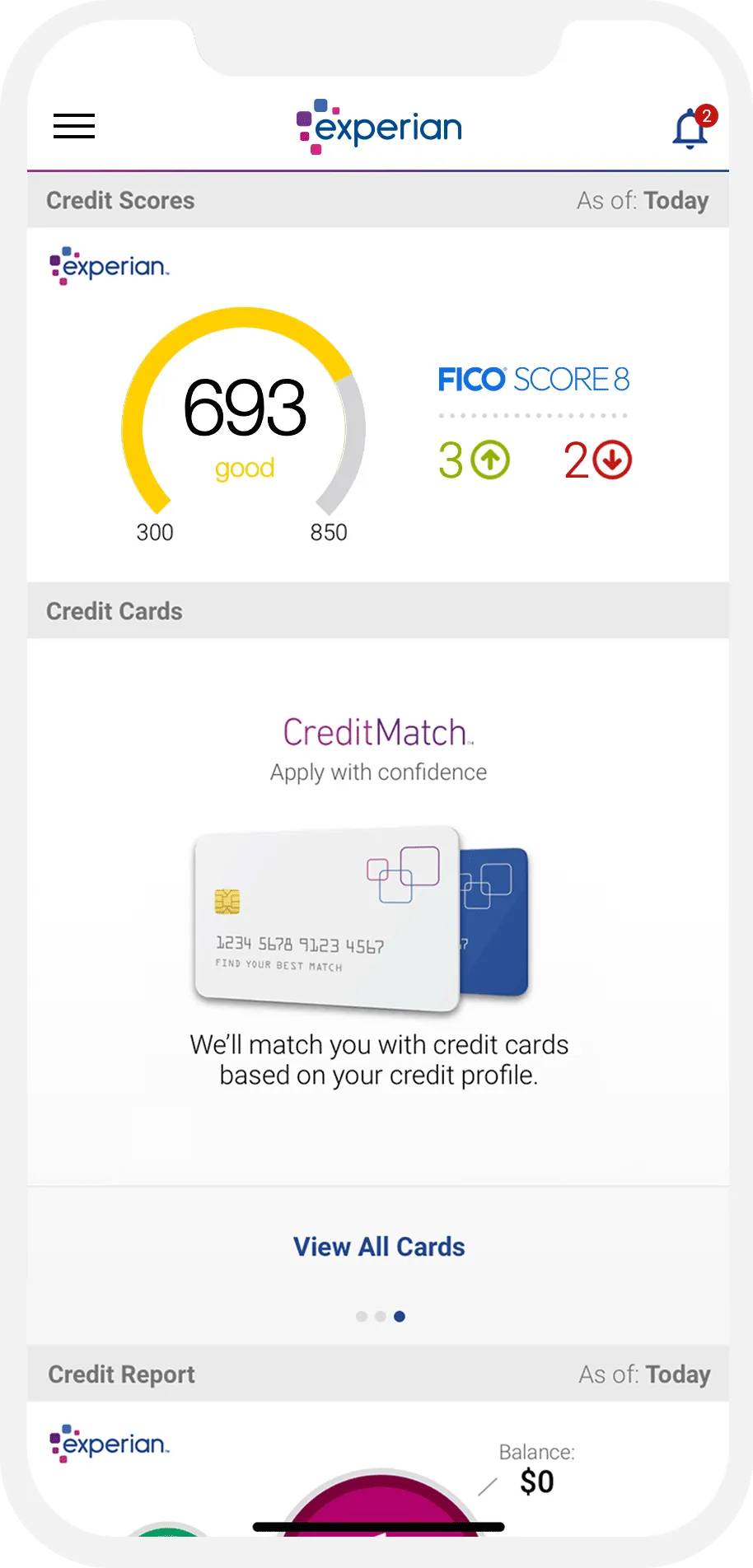

Experian – When You Want the “Real” Stuff

Here’s where it gets interesting. Experian gives you actual FICO scores for free, which is kind of amazing when you think about it. This is the same score your mortgage lender probably uses.

I started using their app after getting tired of the VantageScore vs FICO confusion. The difference can be significant – I’ve seen gaps of 40+ points between the two scoring models.

Major Wins:

- Real FICO 8 score for free

- Experian Boost actually works (added 12 points to my score)

- Detailed credit report breakdowns

- Dark web monitoring in paid tiers

The Annoying Parts:

- App can be sluggish sometimes

- Constant upgrade prompts

- Only Experian data unless you pay

Actually, let me tell you about Experian Boost real quick. I was skeptical because it sounded too good to be true. But I connected my bank account, and it added my Netflix, Spotify, and utility payments to my credit history. Boom – instant score increase. Not huge, but every point counts when you’re trying to qualify for better rates.

myFICO – For the Data Nerds

So myFICO is where you go when you want ALL the data. Like, all of it. They show you every FICO variant – and there are apparently 28 different versions because why would anything be simple?

I’ll be real with you – this app overwhelmed me at first. There’s FICO Auto Score 8, FICO Bankcard Score 2, FICO Mortgage Score… it’s a lot. But if you’re applying for a major loan, this is incredibly valuable.

Why I Keep It:

- Every FICO score variant

- Three-bureau monitoring

- Score simulators are surprisingly accurate

- Premium identity monitoring

The Downsides:

- Expensive ($19.95-$39.95/month)

- Interface feels dated

- Information overload for casual users

Here’s when I found myFICO worth the cost: when I was shopping for a mortgage. My lender used FICO Score 5, which was 15 points different from the FICO 8 I was seeing elsewhere. That difference nearly cost me a better rate.

The Cost Breakdown (Because Money Matters)

| App | Free Version | Paid Plans | Best Value |

|---|---|---|---|

| Credit Karma | Full access | None needed | Free tier |

| Experian | Basic FICO + report | $24.99/month | Free tier |

| myFICO | Limited | $19.95-$39.95/month | Basic plan if you need FICO |

| Credit Sesame | TransUnion monitoring | $15.95/month | Free tier |

| MoneyLion | VantageScore | $19.99/month | Free if you use other features |

Honestly? Start with the free versions. Most people don’t need to pay for credit monitoring unless you’re dealing with active fraud or preparing for a major purchase.

Identity Theft Protection: Do You Actually Need It?

Real talk: I pay for identity monitoring now, but only after getting burned. If you’ve never had issues, the free monitoring might be enough.

The paid identity protection features vary a lot between apps. Some give you $1 million in insurance (which sounds impressive but is mostly marketing), others focus on dark web monitoring, and a few offer credit freezing tools.

What actually helped me when my identity got stolen wasn’t the insurance – it was having someone to call who knew how to handle the paperwork. If you go with paid protection, make sure they offer real human support, not just automated systems.

Setting Up Your Monitoring (The Right Way)

Okay, here’s my step-by-step process for setting this up without going crazy:

- Start with one free app. I recommend Experian or Credit Karma. Don’t overwhelm yourself with five different apps sending you alerts.

- Turn on mobile notifications but be selective. You want fraud alerts, not “your score went up 2 points” spam.

- Set a monthly review reminder. I check everything on the 1st of each month. Takes about 10 minutes.

- Understand the difference between VantageScore and FICO. They use different algorithms and can vary significantly.

- Don’t obsess over small changes. Credit scores fluctuate. A 5-point drop isn’t the end of the world.

Also, and this might be obvious but I’ll say it anyway – make sure you’re using the official apps. There are sketchy knockoffs that just want your personal information.

What I Learned from Two Years of Testing

The biggest surprise? Most apps are pretty similar in terms of basic monitoring. The differences come down to user interface, additional features, and how quickly they send alerts.

Credit Karma wins on simplicity and being completely free. Experian wins on providing actual FICO scores without charge. myFICO wins if you need comprehensive data and don’t mind paying for it.

“The best credit monitoring app is the one you’ll actually use consistently. A perfect app that sits unused is worthless.”

I currently use three apps: Credit Karma for daily monitoring, Experian for my “real” FICO score, and myFICO when I’m shopping for loans. Overkill? Maybe. But my credit has never been in better shape.

For most people, I’d recommend starting with Experian’s free app. You get legitimate FICO monitoring without paying anything, and you can always add more apps later if needed.

Frequently Asked Questions

Does checking my credit score hurt my credit?

Nope. When you check your own score through these apps, it’s a “soft inquiry” that doesn’t affect your credit at all. You can check it daily if you want (though that’s probably excessive).

Why are my scores different across apps?

Different apps use different scoring models and pull from different credit bureaus. VantageScore 3.0 (used by Credit Karma) often differs from FICO Score 8 (used by Experian). Both are “correct” – they’re just different calculations.

How often should I check my credit score?

Monthly is plenty for most people. I check mine weekly, but I’m probably more paranoid than necessary after my identity theft experience.

Are the free apps really free?

Credit Karma and Experian’s basic monitoring are legitimately free. They make money by recommending credit cards and loans, not by charging you monthly fees.

Should I pay for credit monitoring?

For most people, free monitoring is sufficient. Consider paid services if you’ve been a victim of identity theft, have complex credit needs, or are preparing for major purchases like a house.

My Final Recommendations

After testing dozens of apps and dealing with real credit issues, here’s what I actually recommend:

For beginners: Start with Experian’s free app. Real FICO score, decent alerts, no cost.

For comprehensive monitoring: Use Credit Karma + Experian free apps together. Covers all three bureaus between them.

For data nerds: myFICO if you can justify the cost and want every possible score variant.

For identity theft survivors: Consider paid monitoring from Experian or IdentityForce with human support.

Look, your credit score affects everything from apartment rentals to job applications. It’s worth spending a few minutes setting up proper monitoring. You don’t need to become obsessed with it, but you should know what’s happening with your credit profile.

The peace of mind is worth it. Trust me on this one.

Start with one app, set up your alerts, and check in monthly. Your future self will thank you when you catch problems early instead of discovering them during a loan application.